Table of Content

A great score to buy is much different than the credit score needed to buy. With an excellent credit score, you will get the best rates. If you buy a fixer-upper home, an FHA 203k loan could be an excellent option.

Some private lenders offer this too—but it will vary depending on the lender. The higher your down payment, the more likely you are to qualify for a loan with a low interest rate, too. As you will learn in this section, credit scores are just one of the things they look at to know if you qualify for a loan. Furthermore, your credit score greatly affects your total mortgage costs due to the down payment amount and the interest rate that you will be given depending on your score. Prospective home buyers should aim to have credit scores of 760 or greater to qualify for the best interest rates on mortgages. If you’re wondering what credit score is needed to buy a house, it’s important to remember that the minimum score varies from lender to lender.

Ways to increase a credit score before a home purchase

To help offset this risk, lenders will typically charge borrowers with bad credit higher interest rates. They might also require that such borrowers come up with larger down payments. Credit scores help lenders assess the creditworthiness of borrowers and evaluate their lending risk. And here’s everything you need to know about minimum credit score for home loan in Australia. We think it’s important for you to understand how we make money.

The Department of Veterans Affairs has this great job benefit for our veterans and those on active duty, and we are telling you, there are just no better offers elsewhere. Select independently determines what we cover and recommend. We earn a commission from affiliate partners on many offers.

Can I Get a Mortgage With a Bad Credit Score?

Millennials and Gen Xers are set apart because they have higher average mortgage balances compared to other generations. Below, you can see the average TransUnion VantageScore 3.0 credit score of Credit Karma mortgage-holders in each state (plus Washington, D.C.). If you find errors, report them to the bureau concerned, and you could see a quick increase in your score. Getting a free copy of your credit report is a no-brainer before buying a home. Remember, besides your monthly payment, you’ll have other expenses that come with homeownership.

If your score is below 620, lenders either won’t be able to approve your loan or may be required to offer you a higher interest rate, which can result in higher monthly payments. The baseline credit score that mortgage lenders will consider is a minimum score of 500 . But that’s a low score in their view, and it will limit you to certain types of loans, likely with higher interest rates. To be able to access better mortgage products, a better minimum score is 620. To understand your credit score, it is necessary to acknowledge that it serves as an indicator for mortgage lenders.

Can I get a home loan with bad credit?

There is also a maximum population requirement in order to use this financial product. A mortgage lender is likely to have a minimum credit score of 640 to get a home loan. While the lowest acceptable credit score from the VA isn’t set, the lender you use may have their own minimum that you will need to meet to qualify. With most mortgage lenders, the lowest credit score with a VA mortgage is 580.

Sometimes credit rating bodies record erroneous information, especially about repayment history, which can bring your score down. However, getting the best interest rate also depends on your debt-to-income ratio. If you are over-leveraged, the lender may still charge a higher interest rate to reduce the lending risk. This is an excellent score and makes you an extremely creditworthy borrower. You will enjoy significant negotiating power, and lenders may agree to give you the loan at a much lower interest rate.

Start with our Bond Calculator, then use our Bond Indicator to determine what you can afford. Finally, when you’re ready, you can apply for a home loan. It’s a good idea to get your credit card debt down first and keep the balances low because credit cards often carry the highest interest rates. Make sure you don’t apply for more than one loan at a time because that will signal lenders that your financial status has deteriorated.

Over the life of the mortgage, the cost with interest alone is $303,601 at 3% and $344,016 at 4%. Since more people will actually want to buy properties in more urban areas, this next loan type is more popular, especially for first-time homebuyers. Use a credit builder app — StellarFi helps build credit through positive payment history by reporting all recurring bills to Experian®, TransUnion®, and Equifax®.

Interest rate and program terms are subject to change without notice. Mortgage, home equity and credit products are offered by U.S. A counselor may suggest a debt management plan that eliminates debt in 3-5 years. You make a fixed monthly payment to the credit counseling agency, which pays your creditors after working with them to lower interest rates.

Even though it may signal some negative remarks in your credit report, you may still have a chance to get approved for a home loan. We analyzed the accounts of about 29 million Credit Karma members with mortgages who had been active on the site within the last 36 months. Averages were based on information from members’ TransUnion credit reports from the 90 days previous to the data pull, which occurred on Aug. 13, 2022.

As far as credit mix is concerned, having a variety of account types on your credit report can work in your favor. If you only have credit cards open, you might want to consider opening an installment loan . And if you only have installment accounts open, you might want to add some revolving credit cards to your report instead. Here are the minimum credit scores you typically need to surpass when you fill out a mortgage application. Mortgage lenders can more confidently approve VA loans with lower interest rates since government agencies back these.

Department of Veterans Affairs loans or conventional loans through a private lender that are insured through Freddie Mac or Fannie Mae. The Federal Housing Administration’s program reduces the risks to lenders, so they are happier to take on borrowers with lower credit scores. To help homebuyers further, they allow down payments as low as 3.5% and the chance to refinance when you haven’t paid down much of the mortgage. Conventional loans don’t offer the same protection for lenders, so their credit score requirements are higher. Most conventional loans require a minimum credit score of 620, and a score above 640 is recommended for USDA loans. These minimums are flexible, if, for example, you have a sizable down payment.

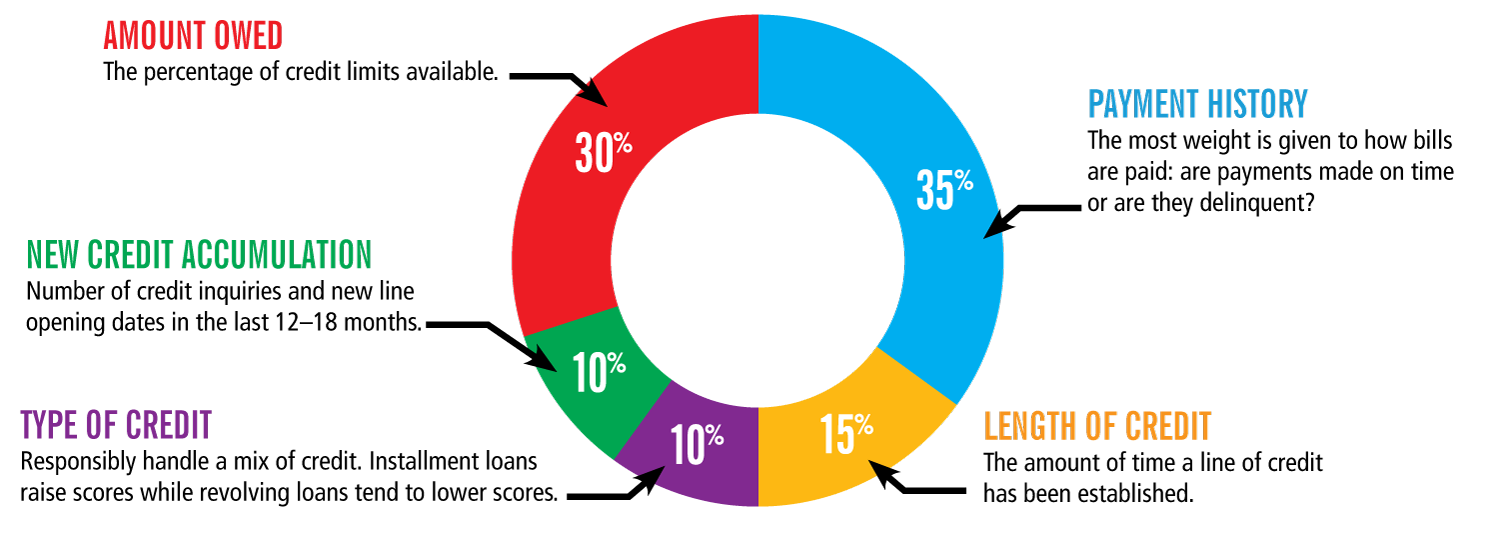

With the FHA 203k mortgage, you can role the cost of repairs needed for a home into one primary loan. The credit scoring requirements for an FHA 203k are the same as a standard FHA loan. Having a higher score could allow you to get a loan with less money down and offer better payment options. As you’ve probably guessed, your credit score is one of the essential factors in purchasing a house. The mix of credit you’ve taken out contributes 10% to your score, as well. Lenders view a credit card, that has nothing to secure it, differently than an auto loan, which has physical property as collateral.

And this example doesn’t even touch on how much a lender might charge you for a mortgage if your credit score falls below 620. You might pay even more to purchase a home with FICO Scores in the bottom of the fair credit score range , assuming you can find a lender that’s willing to approve you. Conventional loans are issued by private lenders, like banks or credit unions. There’s no government agency in the background, like the Federal Housing Administration or the Veterans Administration, that guarantees the loan. How a higher credit score could impact your mortgage loan. Today, there are already many resources, especially online, where you can get free assistance for getting your credit report.

No comments:

Post a Comment